High yield bonds: No longer junk but still high yield

The high yield bond market has undergone a structural transformation since the Global Financial Crisis, reshaping quality, fundamentals, and issuer profiles. Explore how today’s high yield landscape offers compelling risk-adjusted returns and a differentiated role within leveraged finance allocations.

Within fixed income, high yield bonds reflect an area of credit that has been structurally transformed. The evolution of the high yield market is evident when viewing the quality of the asset class by rating, fundamentals and issuer characteristics. These market shifts operate in tandem with portfolio allocation criteria – liquidity, correlation and risk-adjusted returns.

This paper outlines how the high yield bond market has fundamentally changed since the Global Financial Crisis and how it compares to other markets within leveraged finance. High yield bonds offer attractive risk-adjusted returns with features that can limit downside risks while offering total return potential through active management.

THE EVOLUTION OF HIGH YIELD

The high yield bond market originated in the 1980s as the primary financing tool for leveraged buyouts, with banks aggressively underwriting highly leveraged transactions and using high yield bonds as the subordinated, last piece of leveraged buyout (LBO) capital structures. This continued through the 2000s until the 2008 financial crisis triggered sweeping regulatory changes, including the 2013 Leveraged Lending Guidelines and Dodd-Frank reforms, which imposed stricter underwriting standards, leverage limits and higher capital requirements on banks.

These regulatory guardrails fundamentally transformed the market, resulting in a significant quality shift: today’s high yield market features lower average leverage multiples, stronger credit profiles (more BB/B versus CCC-rated issuers), and broader issuer purposes beyond pure LBO financing, while the broadly syndicated loan and private credit markets have absorbed much of the riskiest LBO activity that once dominated high yield issuance.

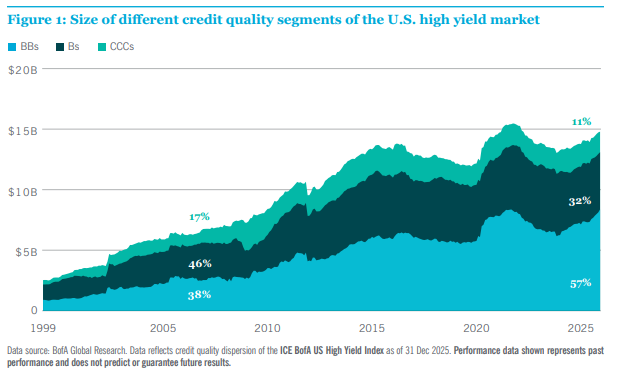

When we view the high yield market by quality, it is apparent that the rating-cohort composition has fundamentally changed. Prior to 2008, the high yield market had a BB-rated composition of roughly 38% and a CCC-rated composition of roughly 17%. This is a notable departure when we look at the current composition, which stands at roughly 57% BB-rated and 11% CCC-rated (Figure 1).

Fifteen years ago, in the aftermath of the financial crisis, the high yield market was heavily populated by private equity-backed companies resulting from LBOs, often smaller and mid-sized businesses with aggressive capital structures, higher leverage ratios and lower interest coverage. Today, the high yield market increasingly features larger, established public companies with investment-grade operations but non-investment-grade ratings. These issuers tend to be well-capitalized with stronger balance sheets, lower leverage multiples and healthier interest coverage ratios.

The shift reflects both regulatory constraints on aggressive LBO financing and broadening of the asset class to include more operating companies accessing the market for general corporate purposes, refinancing or strategic acquisitions rather than pure financial engineering. The public versus private composition has shifted toward more public issuers as the broadly syndicated loan market and the upper-middle market of private credit have captured much of the private equitybacked, highly leveraged financing that once

dominated high yield bond issuance.