What CLO investors should know in 2026

As credit markets navigate evolving conditions, CLOs continue to capture investor attention. Hear from Nuveen’s structured credit leaders on what’s shaping the CLO landscape and what opportunities may unfold in 2026.

Himani Trivedi, head of structured credit at Nuveen, and Tracey Jackson, CLO Client Portfolio Manager, explore the evolving CLO market and the outlook for 2026: the impact of interest rate changes on returns, ETF flows, captive equity trends, and spread compression across the capital stack—and how investors should position for tight arbitrage while preserving equity value.

Q: HOW WILL THE FEDERAL RESERVE’S SHIFT FROM RATE HIKES (2022-2024) TO RATE CUTS AFFECT CLO INCOME OPPORTUNITIES?

A: Collateralized loan obligation (CLO) equity returns are driven by a combination of ongoing income generation and terminal value, and lower rates can be constructive across several imensions.

Credit fundamentals generally improve as borrowing costs decline. Higher base rates over the past few years increased interest burdens for issuers, pressured leverage metrics, constrained free cash flow and limited companies’ ability to invest in operations or pursue M&A. A lower-rate environment alleviates these pressures, supporting liquidity and in many cases, improving credit quality at the underlying borrower level.

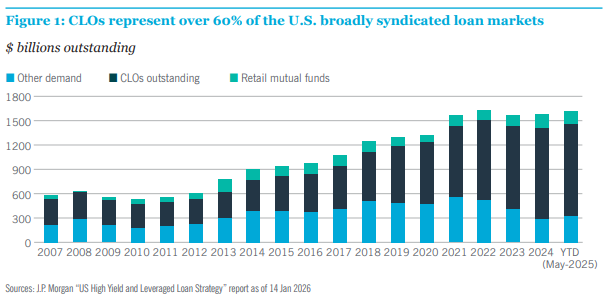

From a broader market perspective, declining ates could help stabilize or potentially reverse the credit deterioration observed over the past couple years. Given CLO equity is levered exposure to corporate debt, this improvement in credit fundamentals can be a return tailwind if defaults decline or stressed loans appreciate in price. Additionally, with private equity dry powder on the sidelines, the improved conditions and lower financing costs may catalyze leveraged buyout activity. This, in turn, could drive higher loan issuance in 2026, supporting growth in both the broadly syndicated loan market and CLO markets (Figure 1).

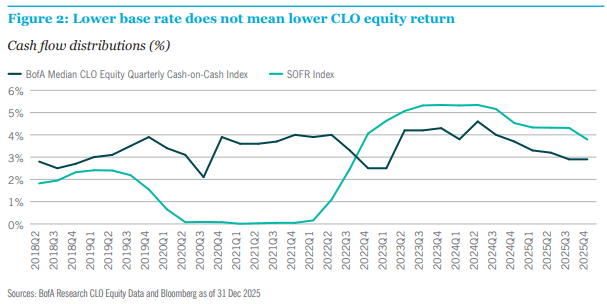

Importantly, CLO equity cash flows are largely insulated from rate cuts. In most structures, approximately 90% of rate decline will be netted between floating rate assets and liabilities. History shows that CLO equity cash-on-cash distributions have remained robust even in very low-rate environments. As illustrated in the chart, from 2020-2022, when the Secured Overnight Financing Rate (SOFR) was near zero, median CLO equity quarterly cash-on-cash distribution remained in the ~3-4% range (Figure 2).