One Economy, Three Cycles

Investing Across a Multi-Speed World

At first glance, today’s global economy appears deceptively straightforward. Growth has proven resilient, labor markets, while softening, remain intact, and despite the Middle Eastern conflict, risk assets continue to be well behaved. Yet beneath the surface, a more complex reality is unfolding.

We are not operating in a single, synchronized economic cycle. Instead, we are navigating one economy, but three distinct cycles, each moving at its own speed, driven by different forces, and carrying unique implications for investors.

Understanding this divergence is central to how portfolios should be constructed in a world where aggregate data obscures increasingly important dispersion.

The Three Cycles

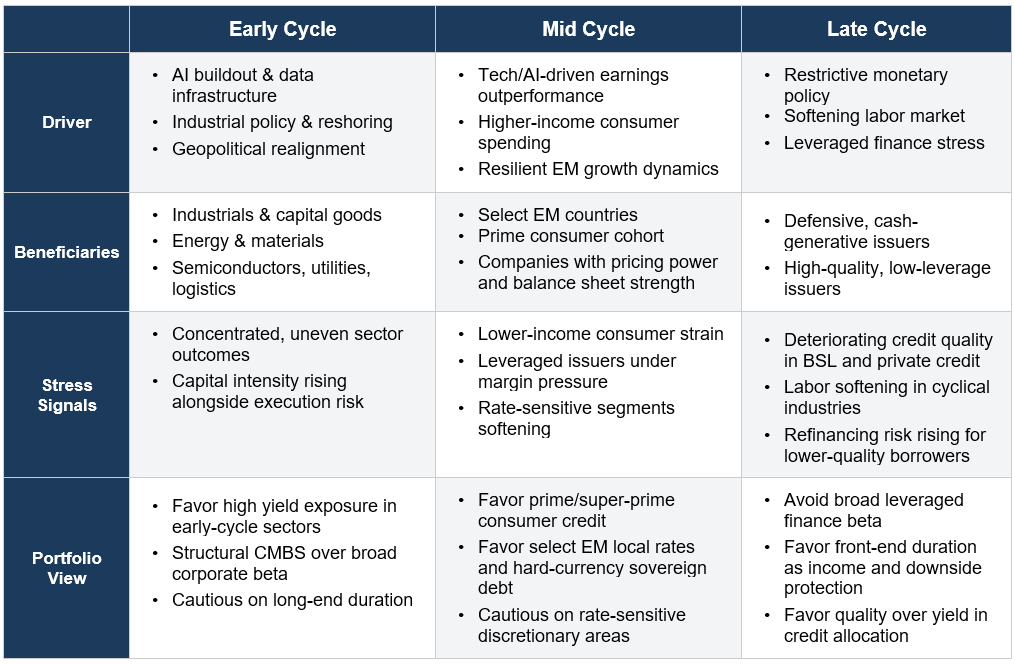

The Early Cycle: Capex, AI, and Industrial Policy

The first cycle is unmistakably early-stage, driven by a surge in capital investment tied to artificial intelligence, infrastructure modernization, and reshoring. Governments and corporations are deploying capital at scale, catalyzed by geopolitical competition, supply chain realignment, and technological transformation.

This is not a traditional recovery. It is a structurally supported, capital-intensive cycle with longer duration and greater policy backing than a typical expansion.

The beneficiaries are clear and concentrated. Industrials and capital goods tied to physical buildout: construction and equipment are at the center. Materials and energy-adjacent industries are benefiting from sustained demand linked to electrification, data infrastructure, and domestic production.

The digital infrastructure ecosystem, semiconductors, data centers, and power inputs, is also becoming more capital-heavy, creating second-order effects across utilities and grid investment. Transportation and logistics are seeing tailwinds as supply chains shift toward resiliency over efficiency.

Importantly, this cycle is defined by targeted capital flows rather than broad-based growth, resulting in increasingly uneven outcomes across sectors.

The Mid Cycle: Resilient but Narrow Growth

Overlaying this is a mid-cycle expansion characterized by positive but increasingly narrow growth. Aggregate activity remains firm, but the drivers of that strength are concentrated.

Technology and AI-linked sectors continue to outpace the broader economy, benefiting from both cyclical resilience and structural tailwinds. Their outsized contribution masks a more uneven underlying landscape.

Consumer dynamics are increasingly segmented. Higher-income households remain supported by asset appreciation and stable employment, sustaining demand in travel, leisure, and premium goods. Lower- and middle-income cohorts are facing pressure from elevated borrowing costs and persistent price levels, leading to softer discretionary spending.

This divergence is evident across retail and consumer-facing industries, where essential categories remain stable while more rate-sensitive segments show signs of strain.

At the same time, emerging markets are reasserting themselves as a meaningful source of growth, supported by improving domestic fundamentals, more orthodox monetary policy, and exposure to global trade and commodity flows tied to the early-cycle capex dynamic.

Within corporate sectors, dispersion is also widening. Companies with pricing power and strong balance sheets continue to perform well, while more leveraged issuers face margin pressure and refinancing risk. The result is a mid-cycle phase that appears stable on the surface but is increasingly defined by selective growth beneath it.

The Late Cycle: Policy Friction and Emerging Stress

At the same time, elements of a late-cycle dynamic are emerging, particularly in labor markets and more leveraged parts of the economy.

Monetary policy remains restrictive, creating a lagged tightening effect that is increasingly visible beneath the surface of aggregate data.

Labor markets, while still solid at a headline level, are beginning to diverge. Larger firms and sectors tied to structural growth remain stable, but pockets of softness are emerging across smaller businesses and more cyclical industries. Hiring has slowed, wage growth is moderating, and the savings rate has gradually declined.

More notably, stress is building within leveraged finance. Tighter financial conditions are weighing on interest coverage, particularly for lower-quality borrowers. In broadly syndicated loans, credit quality has deteriorated over time, while in private credit, exposure is often concentrated in more leveraged sectors.

Certain industries, notably parts of technology and software, are facing a more complex backdrop, as higher capital intensity, evolving AI-driven disruption to traditional business models, and elevated leverage intersect with tighter financing conditions.

This is not yet a broad-based downturn. Rather, it is a selective emergence of stress concentrated where leverage, financing needs, and weaker fundamentals intersect. The late cycle, in this context, is not an endpoint, but a coexisting layer within a broader system.

Investment Implications:

From Beta to Precision

The coexistence of these three cycles creates a fundamentally different investment landscape. Traditional approaches that rely on broad exposure are less effective in a world defined by dispersion.

Instead, the emphasis shifts toward precision.

Within credit, this favors idiosyncratic opportunities over broad beta. In high yield, widening dispersion supports selective exposure to industries benefiting from early-cycle tailwinds, while avoiding more challenged, rate-sensitive segments.

In securitized markets, structural features and collateral quality provide differentiated exposure to areas supported by stable cash flows, with select opportunities in segments such as commercial mortgages where security selection and structure can help mitigate underlying market pressures.

At the same time, there is an increasing preference for interest rate exposure relative to credit, particularly at the front end of the yield curve. Front-end rates offer a more attractive balance of income, liquidity, and downside protection, while also serving as a more reliable hedge as late-cycle risks begin to emerge.

Emerging markets also play a more important role. Select countries offer attractive real yields, improving policy credibility, and exposure to global growth dynamics, creating opportunities across both local rates and currency markets.

Across all these areas, the opportunity set is increasingly defined not by where the market is, but by where capital is flowing, where fundamentals are holding, and where stress is beginning to emerge.

In a world of one economy and three cycles, the objective is not to position for a single outcome, but to build portfolios that are resilient across multiple, coexisting realities.

Investment in foreign securities entails certain risks from investing in domestic securities, including changes in exchange rates, political changes, differences in reporting standards, and, for emerging market securities, higher volatility. Investing in high-yield securities entails certain risks from investing in investment grade securities, including higher volatility, greater credit risk, and the issues’ more speculative nature.

This material reflects the firm’s current opinion and is subject to change without notice. Sources for the material contained herein are deemed reliable but cannot be guaranteed. This material is for illustrative purposes only and does not constitute investment advice or an offer to sell or buy any security. Past performance is no guarantee of future results.

This material has been approved by Payden & Rygel Global Limited which is authorised and regulated by the Financial Conduct Authority. This material has been approved by Payden Global SIM S.p.A. which is authorised and regulated by CONSOB.[SO1]

[SO1]If being distributed to UK/EU.